Blockchain Goes To Work At Walmart, IBM, Amazon, JPMorgan, Cargill and 45 Other Enterprises

As originally publishe on: forbes.com

On the Jersey side of the Hudson River just across from Manhattan’s Financial District, there is a glass-and-steel office tower designed in a severe International Style aesthetic. “DTCC” is emblazoned across the top, but few outside of Wall Street realize that in this building, occupied by the Depository Trust & Clearing Corp., are records for most of the world’s securities, representing some $48 trillion in assets—from stocks and bonds to mutual funds and derivatives. In the 1970s, Wall Street created a DTCC predecessor to replace a system that had been powered by young men running around the cavernous alleys of lower Manhattan delivering stock certificates from brokerage house to brokerage house.

DTCC still has paper certificates in its vaults, but records related to the 90 million daily transactions it handles are kept electronically on its servers and backed up in various locations. Thousands of financial institutions and exchanges in 130 countries rely on DTCC for custody, clearing, settlement and other clerical services.

In a few months DTCC will begin the largest live implementation of blockchain, the distributed database technology made popular by the bitcoin cryptocurrency. Records for about 50,000 accounts in DTCC’s Trade Information Warehouse, where information on $10 trillion worth of credit derivatives is stored, will move to a customized digital ledger called AxCore.

According to Rob Palatnick, DTCC’s chief technology architect, the warehouse already keeps an electronic “golden record” of events such as maturity dates, payment calculations and other activities needed to clear and settle these securities daily. But each participant in a complicated credit derivatives transaction also keeps its own records, which must in turn be reconciled multiple times before the investment matures. By moving those records to the blockchain, visible to all participants in real time, most of those redundancies won’t be necessary.

“We’re not talking about eliminating humans and firms,” Palatnick says. “We’re talking about getting rid of layers of databases and translations between those databases.”

On the other side of the world, in Taipei, Taiwan, Foxconn, the electronics giant best known as a manufacturer of iPhones, launched a Shanghai startup called Chained Finance with a Chinese peer-to-peer lender. Chained will soon connect Foxconn and its many small suppliers (and their suppliers’ suppliers) on an Ethereum-based blockchain that will use its own token and smart contracts (read: automatically executed) to make payments and provide financing in near real time, eliminating a daisy chain of paperwork.

“We view blockchain as the skeleton of our work,” says Jack Lee, the founder of Foxconn’s venture capital arm, which has invested $40 million in six blockchain startups. “Smart contracts that automatically execute transactions are the muscles, and tokens are the blood.”

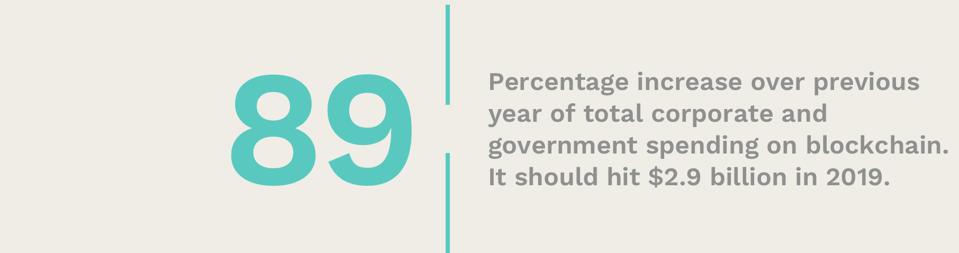

Welcome to the brave new world of enterprise blockchain, where corporations are embracing the technology underlying cryptocurrencies like bitcoin and using it to speed up business processes, increase transparency and potentially save billions of dollars. At its core, blockchain is simply a distributed database, with an identical copy stored on many computers. That facilitates transactions (financial or otherwise) between individuals (or companies) that don’t know or trust each other. It’s virtually impossible to cheat, since every transaction is recorded in many places and the details of those transactions are visible to everyone. Companies are already using blockchain to track fresh-caught tuna from fishing hooks in the South Pacific to grocery shelves, to speed up insurance claims and to manage medical records. Total corporate and government spending on blockchain should hit $2.9 billion in 2019, an increase of 89% over the previous year, and reach $12.4 billion by 2022, according to the International Data Corp. When PwC surveyed 600 “blockchain-savvy” execs last year, 84% said their companies are involved with blockchain.

To chronicle the rise of so called “enterprise” blockchain, Forbes has created its first annual Blockchain 50 list of big companies that are putting the technology to work in meaningful ways. While blockchain’s first application, cryptocurrency, is struggling to achieve mainstream adoption, these companies are committing manpower and capital to build the future on top of shared databases.

The version of a blockchain future these companies are building is, for the most part, far different from what the founders and early adopters of blockchain had envisioned. While many cryptocurrency idealists fantasize about a global, public network of individuals connected directly and democratically, without middlemen, these companies—many of which are middlemen themselves like DTCC—are building private networks they will use to profit from centralized management.

Not surprisingly, financial firms—from Allianz to Visa and JPMorgan Chase—dominate the list. But Blockchain 50 companies run the gamut of industries, including energy firm BP, retailer Walmart and media company Comcast.

Because of the lingering bad taste left by bitcoin drug bazaars like Silk Road and the 2017 digital currency bubble, most companies emphasize the distinction between crypto and blockchain, shunning the former and embracing the latter. In some ways the members of the Blockchain 50 represent a bridge between the old and new worlds. Just as internal computer networks were adopted by companies long before the internet took off, these firms are starting by adopting distributed ledger technology at a small scale.

“The era of blockchain tourism has ended,” says Bridget van Kralingen, Senior Vice President for Platforms & Blockchain. “We’ve really seen blockchain move from being overshadowed by cryptocurrency to focus on real business problems and complex processes.”

In 2009, when Satoshi Nakamoto, bitcoin’s pseudonymous creator, activated his network, its blockchain was the underlying accounting system that let anyone with bitcoin transfer money without the need of a middleman. Transactions are processed in blocks—just a fancy word for a hunk of data—about every ten minutes, each containing a compressed version of the previous block, linking them together into a chain. Instead of relying on a bank or another middleman to keep track of when a bitcoin leaves one location and arrives at another, the thousands of computers on the bitcoin network do the work and in exchange for their efforts are paid in bitcoin.

For most companies this presented a potential problem. While identities aren’t required to use the bitcoin blockchain, the transactions themselves are tied to addresses that are publicly available, meaning that with a bit of work many of these addresses can be tied to actual people or companies. Thus enterprises like Coca-Cola and JPMorgan Chase, accustomed to maintaining competitive advantages based on proprietary processes and control, were initially skeptical of cryptocurrency.

Businesses also need some control over their data. “The entire corporate world has been fashioned around who has responsibility over a particular part of the business flow,” says David Treat, the global head of Accenture’s Financial Services Blockchain practice. “There can be no gaps, because that is unacceptable for a multibillion-dollar company. You cannot have a gap, or you are subject to huge security breaches and social contract breaches.”

Perhaps no firm has had a greater influence on the growing corporate use of blockchain technology than Digital Asset Holdings, a New York-based startup that hired the former JPMorgan Chase banker Blythe Masters as its CEO in early 2015. Under Masters, Digital Asset began making acquisitions and almost immediately purchased a small company that was in the process of building an “invitation only,” or permissioned, blockchain. Then in late 2015 Digital Asset donated the code for its “open ledger” project to the Linux Foundation, which supports commercial open-source software projects, including the Linux operating system.

The project was called Hyperledger, and thanks in part to Masters’ connections, its backers read like a who’s who of finance and technology. Thirty companies are listed as founders, including ABN AMRO, Accenture, Cisco, CME Group, IBM, Intel, JPMorgan Chase, NEC, State Street, VMware and Wells Fargo. Hyperledger immediately established itself as the gold standard for corporate blockchain projects.

What happened next might be considered the Big Bang moment of enterprise blockchain. In early 2016, IBM donated 44,000 lines of code to the project, which formed the core of a new blockchain with faster speeds and increased privacy. No fewer than half of the members of the Forbes Blockchain 50 are now using that blockchain, known as Hyperledger Fabric.

“We’ve been very focused on making sure that not only is the blockchain technology standard but that the documents and data are standard,” says Marie Wieck, IBM Blockchain’s general manager. “This standardization allows [the companies] to not spend their time comparing differences and validity in the documents.”

Shortly after the launch of Hyperledger, which is a nonprofit venture, a New York fintech called R3 raised $107 million from the likes of ING, Barclays and UBS to create a for-profit enterprise blockchain platform called Corda Enterprise.

As the commercial potential of co-opting blockchain technology became more apparent, many cryptocurrency startups began to rethink their models.

For example, San Francisco’s Ripple, originally called OpenCoin and conceived of as yet another alternative monetary system, expanded its focus in late 2015 from the cryptocurrency (called ripple and trading as XRP) to building software for large banks. A bitcoin startup called Counterparty spawned another company, Symbiont, in March 2015, which coded a proprietary blockchain that’s now being used by Vanguard for sharing stock index data. In February 2017, ConsenSys, a Brooklyn-based collection of crypto companies controlled by one of Ethereum’s founders, helped launch the Enterprise Ethereum Alliance.

Just as corporate America co-opted counterculture vibes for its marketing and advertising (“Think Different,” “Don’t Be Evil”), its most forward-thinking businesses are fast incorporating a technology that was designed in large part to eliminate them.

In insurance, for example, MetLife’s mobile app Vitana bundles insurance with a test for gestational diabetes that uses a blockchain to record data and verify and pay claims. In recent testing in Singapore, where one in five expectant mothers develops gestational diabetes, a practitioner simply enters a positive test result into a patient’s electronic medical record and in a matter of seconds MetLife’s smart contract deposits an insurance payment into that patient’s bank account to cover the medical expenses associated with the condition. No paperwork or claim filing necessary.

Similarly, Germany’s Allianz, working with EY, tested moving certain captive insurance claims processes—often involving many emails, attachments and phone calls across multiple times zones—to a private blockchain. The time required to process a claim fell from weeks to hours.

The French bank BNP Paribas, which has lent money to commodities traders since the 19th century, is considering using a ledger platform called Voltron to process letters of credit for traders. Northern Trust has begun administering private equity funds using Hyperledger Fabric. Broadridge Financial has been running pilots testing multiple distributed ledgers for its dominant proxy voting and shareholder communications business.

“In real time, you know who owns the stock, who’s entitled to vote and how it’s tied to the universally-agreed-upon shareholder meeting agenda,” says Michael Tae, Broadridge’s head of strategy.

In the perpetually fraught food business, which regularly endures disasters ranging from E. coli outbreaks to a worker being cooked alive, companies like Nestlé and Bumble Bee Foods are turning to blockchain to secure their supply chains and reduce paperwork.

Golden State Foods, a big McDonald’s supplier that makes more than 400,000 hamburgers per hour, tracks the location and temperature of its patties with devices like radio-frequency ID tags and Hyperledger Fabric. The system can immediately alert GSF to conditions that might lead to spoilage. At the same time, it can optimize inventory levels by tracking how much meat is in a truck or in a restaurant’s freezer, in real time.

At this year’s SXSW conference in Austin, Texas, Bumble Bee unveiled an SAP-built supply-chain blockchain offering complete transparency to its customers. Soon you will no longer have to take Bumble Bee’s word for it when its assures you that the 12-ounce package of yellowfin tuna you just bought was caught by individual fishermen in the South Pacific and not by a factory ship. The fishing crews, tuna processors and packers are now entering their own data in real time on Bumble Bee’s distributed ledger. By summer, Bumble Bee will be sharing that information with retailers and customers who take the time to check.

From a public relations standpoint alone, Bumble Bee’s SAP blockchain is likely to bear dividends. In 2017 Greenpeace ranked Bumble Bee 17th out of 20 tuna brands for its sustainability practices, accusing it of “greenwashing” a host of bad behaviors with environmentally friendly marketing.

“Food safety and sustainably sourced product has become an overwhelmingly important topic in our industry,” says Tony Costa, the CIO at Bumble Bee. “Leveraging the latest technology enables us to open it up to more of a public perspective, if you will. So we get out of the business of managing data. We’re relying on a relationship.”

In the healthcare business, an estimated 20 cents of every dollar—some $700 billion a year—is wasted because of inefficiencies. Ciox, a little-known company based in Alpharetta, Georgia, that manages medical-records exchanges for 60% of the hospitals in the U.S., is considering developing a private blockchain that healthcare providers could use—for a fee paid to Ciox—to exchange data. Blockchain 50 enterprises like Ciox and the media giant Comcast, which is toying with using blockchain to micro-target television advertisements, plan to use the privacy features of blockchain to profit from their customers’ data while protecting their identities.

Despite the surge in corporations working on blockchain projects, the technology is still new, and relatively few have generated significant revenues or savings.

The one group that is getting rich from the current enterprise blockchain gold rush: consultants. Deloitte, PwC, KPMG, EY and Tata Consultancy Services are deploying small armies to preach the virtues of blockchain to the C-suite and charging huge fees to help companies implement the technology. (We excluded consultants from the Blockchain 50 because they played a key role in helping us create the list.) Deloitte, for example, has 1,400 full-time blockchain employees. India’s Tata has 1,000 staffers, 600 of them full-time, in its blockchain unit. Tech firms, including Oracle, SAP and Amazon, are also staking out their turf.

Part technology firm, part consultant, IBM may be the biggest and most successful enterprise blockchain company of all. Besides helping create Hyperledger Fabric, the company has 1,500 staffers—mostly engineers—devoted to the new technology and reports that its IBM Blockchain powers 500 client projects.

IBM Food Trust, for example, counts Walmart, Kroger, Nestlé and Carrefour, the French grocer, among its 50-plus members. IBM is also behind TrustChain, a consortium of companies in the supply chain for diamonds and jewelry, including Rio Tinto Diamonds, Asahi Refining and Helzberg Diamonds. Health Utility Network, another Big Blue group, counts three of the five largest U.S. health insurers—Aetna, Cigna and Anthem—as members.

“The power of any blockchain network is in its participants and its members,” says IBM’s Wieck. It matters little whether those members are crypto-idealists or global corporations.